Is A Balance Transfer Right For You?

12/10/2018

![]() 3 min. read

3 min. read

By: FCU Team

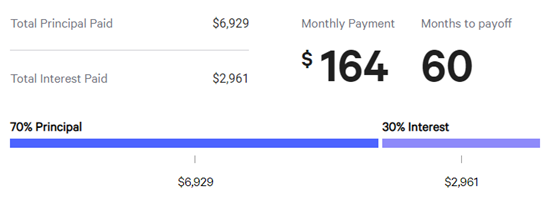

According to NerdWallet the typical American family owes $6,929 in credit card debt. With the average interest rate sitting at 15%, it could take up to seven years to pay down a balance of that size, if you’re just making minimum payments. What many Americans are finding, is that balance transfers provide much needed relief from high interest rates and overwhelming monthly payments. A balance transfer allows you to move existing balances from your current card(s) over to a new card that typically has a special offer and/or a lower rate!

![]()

These special offers and promotional periods offer a window that will allow you to pay your balances down without having to worry about interest. Take a second to review these pros and cons to see if a balance transfer is the right option for you!

Pros

Interest-free Debt

The number one motivator for a balance transfer is escaping the interest that is accruing on your current cards. Depending on the offer, you might be able to do that for up to 21 months. In addition, if your credit score has improved, you could potentially qualify for a better rate once the promotional period ends. Making a balance transfer can allow you to make real progress toward getting out of debt since payments go completely toward your principal balance during the 0% period.

Convenience

The more bills you have to keep track of each month, the greater chance you have of missing a payment. A balance transfer can consolidate the balances from multiple cards to just one. Not only does this decrease the number of monthly payments you need to make but you’ll be decreasing the amount you pay as well.

Financial Freedom

Taking a step toward paying down your debt is also likely to motivate more careful spending habits. What many people start to realize, once they get a balance transfer, is how much of their payment was previously going toward interest. Let’s go back to that $6,929, the average American family has in credit card debt. If you decided to pay this balance off within 5 years, you would end up paying almost 43% in interest alone.

Cons

Fees

Most balance transfer offers charge a minimum of 3-5% of the balance you’re transferring. So, while you may not be incurring any interest, the transfer itself isn’t always free. On top of that, some credit card companies also tack on annual fees, so be sure you read all of the terms and conditions before applying.

Impact on Your Credit Score

Having too many open cards might make lenders view you as a risk so, opening a new card without closing out old ones, could be a bad thing. On the other hand, you will have more available credit, lowering your utilization rate, which is often a huge factor in determining your credit score.

Not Staying Debt Free

If you have enough self-control and can keep the cards that you’re paying off at 0 balances then go for it. Keeping the cards you’ve had the longest open will reflect well for credit bureaus. However, many find it challenging to not use the newly available credit that a balance transfer may present. If you think that it might be a risk for you, it is definitely wise to close out cards once they’ve been paid off.

What's Next...

After weighing the pros and cons of a balance transfer, it’s time for the fun part, shopping! No, not that kind of shopping. It’s time to review your options and see which card is the best fit for you.